This content is for informational purposes only and does not constitute legal advice or create an attorney-client relationship.

Solar energy is one of the most heavily marketed home improvements in the U.S. today.

Ads promise “free solar,” energy independence, and guaranteed savings. But behind the glossy brochures and flashy websites lies a much more complex reality.

The truth is, solar can be a smart investment, but it’s also one of the most abused industries when it comes to misleading contracts, hidden costs, and long-term financial traps.

Before you sign anything, here’s what you need to know about the actual cost of solar, and how to protect yourself to make sure you’re getting a good deal.

1. Upfront Cost vs. Long-Term Cost

One of the most confusing parts of going solar is that there’s rarely a straightforward price tag.

You might hear:

- “$0 down!”

- “Just $79/month!”

- “Free installation!”

- “You’ll never have an electricity bill again!”

But what these offers often mask is that you’re still paying, just over time.

Three main types of solar deals:

- Cash Purchase: You pay the full system cost upfront. Anywhere from $15,000 to $35,000 depending on system size, location, and incentives.

- Loan Financing: You take out a loan (often 20-25 years) to pay for the system. This includes interest and sometimes additional origination fees.

- Lease or Power Purchase Agreement (PPA): You don’t own the system. You pay monthly to “rent” the energy it produces. This often comes with annual price escalators.

Pro tip: If a rep can’t tell you the total system cost in dollars, walk away.

2. How to Calculate the Real Price

To truly understand the cost of going solar, you have to look beyond the teaser rate or “$0 down” pitch and calculate the total financial impact over time.

That includes:

- Interest on Solar Loans: Many loans span 20–25 years with high APRs and hidden finance charges

- Escalators: Lease and PPA payments can increase 2–3% every year

- Maintenance & Monitoring Fees: Often not included in the original quote

- Transfer or Prepayment Fees: Charged when you sell your home or try to pay off the loan early

- Lien Recording Fees: Some lenders file UCC liens without clearly disclosing them

- Warranty Costs: Sometimes sold separately, with limited real coverage

- System Removal Costs: If you need to re-roof or move, removal and reinstall can cost thousands

Here’s what that looks like in real life:

Below are screenshots and quotes from real legal assistants at Prevost Law Firm, working with real prospects who need solar relief.

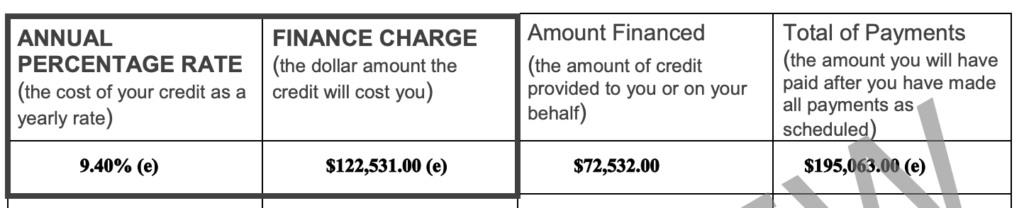

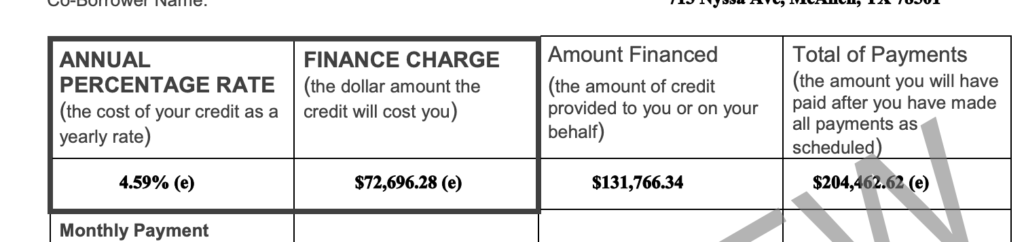

“I think this is the HIGHEST loan I have seen yet — $205,286 + $123,671 in finance charges = $328,958. And it was for 43 panels. That’s it.”

“I see your $75K finance charge… and raise you a $165K finance charge.”

“I’ve got one: $100k loan by a FAMILY FRIEND with an 11.99% interest rate, her total amount after interest is $294k!!!”

“Every client I’ve talked to says this is the worst financial decision they’ve ever made. This isn’t a car they need to get to work or a surgery they need to live. The salespeople were serpents.”

“Predatory sales tactics, high pressure sales tactics, preying on people’s lack of understanding. It’s disgusting the stories we hear every day…”

“One client’s payments are about to jump to $777/month—and they had no idea until we reviewed the contract.”

If you were never shown a full amortization schedule or finance disclosure, or if the payment escalators and backend fees were glossed over, you may have been misled. These situations aren’t just frustrating. They can have legal implications.

Prevost Law Firm has helped homeowners untangle contracts like these and hold lenders and installers accountable.

Let’s break down a real-world example:

You’re quoted $250/month for 25 years through a solar loan.

At first glance:

- 25 years × 12 months = 300 payments

- 300 × $250 = $75,000 total

But here’s what they didn’t tell you:

- The loan has a 9.99% interest rate

- There’s a $90,000 finance charge

- There are payment escalations starting in year 2

- You’re also responsible for monitoring, maintenance, and warranty fees

After 18 months, your monthly payment could jump to $500–$700/month.

And by the end of the loan term, your total repayment could exceed $150,000, all for a system that cost less than half that to install.

We’ve even seen contracts where the finance charges alone were over $165,000.

If you’re being offered financing but don’t see a full amortization schedule or the APR and total repayment amount, walk away.

Or better yet, have a lawyer review the contract before you commit.

If you’ve already signed and are now facing these surprise costs, you may have legal options to fight back.

3. Incentives Are Real, but Not Guaranteed

There are federal and state-level incentives that can offset solar costs:

- Federal Solar Tax Credit (ITC): Currently 30% of the system cost

- State/local rebates

- SREC programs in certain states like NJ and MA

But here’s the catch:

- You must owe taxes to use the ITC. If you don’t have tax liability, the credit won’t help you.

- Some sales reps misrepresent this. Telling retirees or low-income homeowners they’ll get $10,000 back when they actually won’t qualify.

Additionally, the 30% federal residential solar tax credit (Section 25D) is being eliminated early under Trump’s “One Big Beautiful Bill” signed on July 4, 2025.

- Prior to this, the credit was set to continue through 2032 under the Inflation Reduction Act.

- Now, homeowners must have their system installed and commissioned by December 31, 2025 to claim the full 30% credit

- After that deadline, the residential solar tax credit disappears entirely. There’s no step-down, no partial credit in 2026.

However, there’s still a tax credit available for systems under leases or PPAs (i.e., where the leasing company, not you, claims the credit):

- That commercial/residential credit (Section 48E) remains available through December 31, 2027, but only on systems where construction starts by July 4, 2026.

Always check with your CPA before assuming you’ll get the full tax credit.

4. Energy Savings Are Not Guaranteed

One of the biggest reasons people go solar is to lower their electricity bills.

But your monthly savings will depend on:

- How well your system was designed

- Your current utility rate (and future rate increases)

- Net metering policies in your area

- Roof orientation and shading

Some systems are oversold or poorly installed, meaning you don’t produce enough to offset your bill. In some cases, homeowners have ended up paying for the solar loan and their utility bill.

Ask the company to show you:

- Projected vs. actual production on past installs

- Real data on your home’s solar potential

- Net metering rules in your state

If they can’t back up their savings claims with data, that’s a red flag.

5. Maintenance and Warranty Pitfalls

A common sales pitch: “The system is maintenance-free!”

Reality: Panels may be low-maintenance, but they’re not no-maintenance. Most solar systems have multiple components that can break down:

- Inverters

- Monitoring systems

- Wiring

- Batteries (if installed)

Ask for:

- The manufacturer warranty on panels and inverters

- The installer’s labor warranty

- Whether third-party warranty providers are involved (and what they actually cover)

Also, many companies go out of business. Who will service your system if the installer disappears?

6. Selling or Refinancing Your Home

This is a major hidden cost most people don’t think about.

If you want to sell your house:

- Buyers may be wary of taking over a solar lease or loan

- You may need to pay off the loan to transfer ownership

- Appraisers may not count the system toward home value

Some homeowners get stuck with systems they can’t move or sell. Then they must negotiate with lenders to get out.

Always ask:

- What happens if I sell?

- Can the loan transfer?

- Are there prepayment penalties?

7. How to Tell If You’re Getting a Good Deal

Here’s a quick checklist to help you avoid scams and get real value:

- Know the total cost (not just the monthly payment)

- Get at least 3 quotes from reputable providers

- Verify state licensing and Better Business Bureau rating

- Ask for proof of savings from real customers in your area

- Read the full contract, including escalators and buyout clauses

- Don’t rush. High-pressure sales is a red flag

- Consult your CPA before counting on tax credits

- Check if your system will overproduce or underproduce

Final Thoughts: Is Solar Still Worth It?

Yes. Solar can still be a great investment. But it’s not a one-size-fits-all solution.

If you plan to stay in your home long-term, can claim the full tax credit, and get a well-designed system with fair financing or cash payment, solar can save you tens of thousands over 20–25 years.

But if you’re dealing with high-pressure sales tactics, misleading terms, or inflated promises, the costs can outweigh the benefits, and you may be stuck with a contract that drains your finances instead of powering your future.

Take your time. Do your research. And remember: great solar deals are transparent, data-driven, and built around your needs, not a quota.

This content is for informational purposes only and does not constitute legal advice or create an attorney-client relationship.